How Much Tax Is Taken From a $100,000 NYC Salary in 2026? (2027 Filing Guide)

Find out how much tax comes out of a $100,000 NYC salary in 2026. See your estimated take-home pay and filing guide for 2027

A $100,000 salary in New York City sounds great on paper. What actually hits your bank account is a different story. Between federal income tax, New York State tax, NYC city tax, and payroll taxes, a significant chunk leaves before you see a dollar.

Want your exact number right now? Enter your income at taxcalculatorny.com and see your full 2026 breakdown in seconds.

Quick Answer: What Is Take-Home Pay on $100K in NYC?

A single filer earning $100,000 in New York City in 2026 can expect to take home roughly $66,900 to $70,000 after all taxes. That means somewhere between $30,000 and $33,000 goes to federal, state, city, and payroll taxes combined.

That range exists because the exact number depends on your filing status, whether you contribute to a 401(k) or HSA, and whether you have any other deductions. The estimates in this article are for a single filer claiming the standard deduction with no pre-tax contributions. If you put money into a 401(k) or health savings account, your take-home will be higher.

What Gets Taken Out of a $100,000 NYC Salary

Most people think of income tax as one thing. It is actually four separate deductions hitting your paycheck at the same time.

Federal income tax is the largest single piece. The IRS taxes your income across progressive brackets, and a $100,000 salary for a single filer lands mostly in the 22% federal bracket after the standard deduction of $15,000.

New York State income tax comes next. NY State has nine brackets for 2026, and a $100,000 salary for a single filer sits in the 5.90% bracket for the portion above $80,650. The effective state rate on the full income works out to around 5.5% to 6%.

NYC city income tax is the layer that separates city residents from everyone else in the metro area. The top city rate is 3.876% on income over $50,000. This is what New Jersey and Long Island commuters do not pay.

Social Security and Medicare, also called FICA taxes, come out of every paycheck regardless of where you live. Social Security takes 6.2% on wages up to $176,100 in 2026. Medicare takes 1.45% with no income cap. These are flat deductions, not progressive.

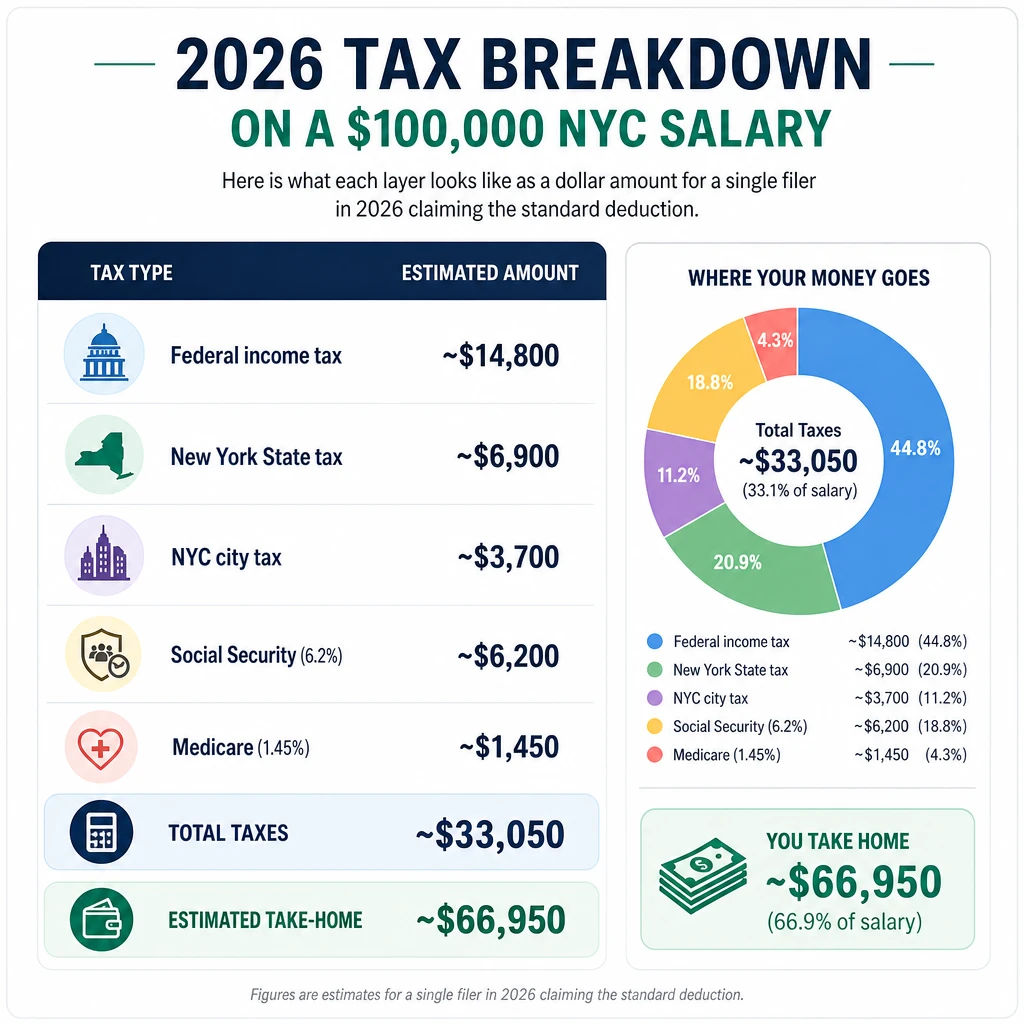

2026 Tax Breakdown on a $100,000 NYC Salary

Here is what each layer looks like as a dollar amount for a single filer in 2026 claiming the standard deduction:

A few things to know about these numbers. The federal estimate accounts for the $15,000 standard deduction reducing your taxable income to $85,000 before the bracket calculation. The state estimate reflects the modest bracket reductions that took effect in 2026 under Governor Hochul's middle-class tax relief. The city tax uses the 3.876% top rate on the portion of income above $50,000 and slightly lower rates on the income below.

Your number might look different if you are married, if you claim dependents, or if you have pre-tax deductions. See what your exact 2026 take-home looks like at taxcalculatorny.com.

Why Your Actual Number Might Be Different

Filing status changes everything. Married filing jointly filers get wider tax brackets at both the federal and state level, which usually means a lower combined bill on the same income. A married couple where one person earns $100,000 and the other earns nothing will generally pay less in total tax than a single filer at the same income.

Pre-tax contributions lower your taxable income. Every dollar you put into a 401(k) comes off your taxable income before federal and state taxes are calculated. Contributing $10,000 to your 401(k) effectively reduces your taxable income to $90,000, which drops your federal, state, and city tax bills. It does not reduce your Social Security or Medicare deductions, but it still makes a meaningful difference. The 2026 401(k) limit is $23,500 for workers under 50.

HSA contributions work the same way. If you had a qualifying high-deductible health plan in 2026, contributions to a Health Savings Account reduce your adjusted gross income before any tax is calculated. The 2026 limit is $4,300 for self-only coverage.

Bonuses and overtime push withholding higher. If you earned $100,000 total but $15,000 of that came from a bonus, your employer may have withheld at a flat federal supplemental rate of 22% on the bonus portion. This can lead to overwithholding during the year and a refund when you file in 2027.

Part-year NYC residency reduces your city tax. If you lived in the five boroughs for only part of 2026, you only owe NYC city tax on the income earned during that period. Someone who moved to the city in July 2026 owes city tax for roughly six months of income, not the full year.

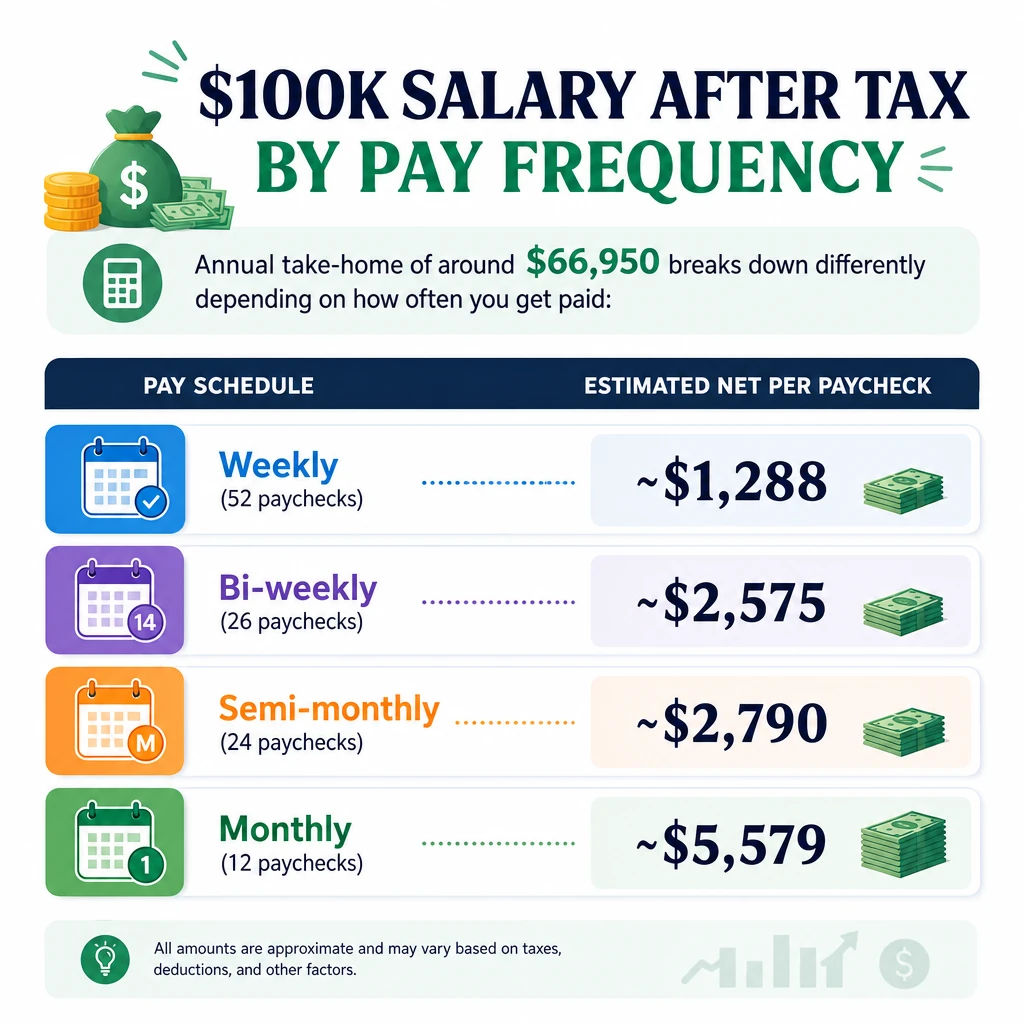

$100K Salary After Tax by Pay Frequency

Annual take-home of around $66,950 breaks down differently depending on how often you get paid:

These figures assume taxes are spread evenly across all pay periods. In reality, withholding can vary slightly depending on when bonuses or commissions are paid and whether your W-4 has any additional withholding instructions.

If your paychecks feel smaller than these estimates, it may mean extra withholding was set up on your W-4, or you have additional deductions like union dues, commuter benefits, or supplemental insurance coming out pre or post-tax.

2026 Tax Rules That Affect the $100K Result

Three things shifted in 2026 that directly affect what a $100,000 NYC earner owes.

New York State updated its withholding tables on January 1, 2026 to reflect the bracket reductions from the 2025-2026 state budget. If your employer applied the new tables on time, your paychecks throughout 2026 were already slightly larger than in 2025 without any action needed on your part.

Federal brackets shifted slightly upward for inflation under the One Big Beautiful Bill Act. This means a small portion of income that would have landed in a higher bracket in 2025 stayed in a lower one in 2026. The practical effect for a $100,000 earner is modest but real.

NYC city tax rates stayed flat. The four city brackets are identical to 2025, so there was no change to the $3,700 city tax estimate from the prior year.

All of these changes are already baked into the estimates above and into the calculator at taxcalculatorny.com, so you do not need to manually adjust for any of them when you run your numbers.

How to Lower the Tax on a $100,000 NYC Salary

There are five practical ways to reduce what you owe before you file in 2027.

Max out your 401(k). Contributing the full $23,500 limit for 2026 would reduce your federal taxable income to around $61,500, which drops your federal bill and your state and city bills along with it. Even contributing $5,000 or $10,000 makes a noticeable difference.

Make a deductible IRA contribution before April 15, 2027. You can still contribute up to $7,000 to an IRA for the 2026 tax year after December 31 has passed. If you qualify for the deduction, this reduces your taxable income for both federal and state purposes.

Check your W-4 withholding. If you have been overwithholding, you are giving the government an interest-free loan all year. Updating your W-4 with your employer can increase each paycheck now rather than waiting for a refund in 2027.

Claim the NYC school tax credit. If your income is under $250,000, you may qualify for this credit, which directly reduces your city tax bill. Many filers miss it because it does not get as much attention as federal credits.

Look at the New York State Earned Income Tax Credit. At $100,000, you may be at or above the income limits depending on your family situation, but it is worth checking. New York State's version of the EITC is worth up to 30% of the federal credit amount for qualifying filers.

When You File This Income: 2027 Deadlines

Income earned in 2026 gets reported on your 2027 tax return. The standard filing deadline is April 15, 2027.

You can request an automatic extension to October 15, 2027, but any taxes you owe are still due by April 15. Filing an extension without paying what you owe will result in penalties and interest on the unpaid balance.

If you expect to owe more than what was withheld from your paychecks, it is worth calculating your estimated liability now so there are no surprises in April.

Frequently Asked Questions

How much take-home pay do I get from a $100,000 salary in NYC in 2026? A single filer claiming the standard deduction can expect roughly $66,900 to $70,000 after federal, state, city, and payroll taxes. The range depends on deductions, filing status, and pre-tax contributions.

Does everyone earning $100,000 in NYC pay the city tax? No. Only people who actually live in the five boroughs owe NYC city income tax. If you live in New Jersey, Connecticut, Long Island, or Westchester and commute in, you skip the city tax entirely and keep an extra $3,700 per year compared to a city resident at the same salary.

Is the tax different if I am married? Yes. Married filing jointly filers generally pay less total tax at the same income level because the federal and state bracket thresholds are wider. The combined bill for a married couple where one partner earns $100,000 will typically be lower than for a single filer at the same income.

Can pre-tax deductions really make a difference? Yes, more than most people realize. Contributing $10,000 to a 401(k) reduces your federal, state, and city taxable income by the same amount. At a combined effective rate of around 30%, that is roughly $3,000 back in your pocket either now through lower withholding or at filing time through a lower bill.

How do I get my exact number for 2026? Enter your income, filing status, and any pre-tax contributions at taxcalculatorny.com. The free calculator applies all 2026 rates across federal, state, and city and gives you your take-home pay in under a minute.

All figures in this article are estimates for a single filer using the 2026 standard deduction with no pre-tax contributions, based on official rates from the IRS, New York State Department of Taxation and Finance, and New York City Department of Finance. For advice specific to your tax situation, consult a licensed tax professional.