2026 NYC Tax Brackets Explained: What They Mean for Your 2027 Return

Confused about NYC tax brackets for 2026? We break down every bracket, what rate you pay, and exactly how it affects your 2027 tax return

If you got a raise in 2026, moved to New York City, or are filing here for the first time, you have probably wondered what tax bracket you are in and what that actually means for your bill. The answer is less scary than most people expect once you understand how brackets work.

Not sure where your 2026 income lands? Enter it at taxcalculatorny.com and see your full federal, state, and city breakdown in seconds.

What Tax Brackets Are (and What They Are Not)

Here is the most common tax mistake people make: assuming that being in a certain tax bracket means their whole income gets taxed at that rate.

It does not work that way. A tax bracket only applies to the income that falls within that specific range. The income below it still gets taxed at the lower rates.

Say you earn $60,000 in NYC. You are not paying the top NYC rate on all $60,000. You pay 3.078% on the first $12,000, then 3.762% on the next chunk up to $25,000, then 3.819% on the amount from $25,001 to $50,000, and finally 3.876% on the remaining $10,000 above that. Each slice gets its own rate. Only the top slice hits the top rate.

This matters because a lot of people hesitate to take a raise or pick up extra work because they think it will push their entire income into a higher bracket. That is not how any of this works. Only the extra dollars above the threshold get taxed at the higher rate. Everything below stays the same.

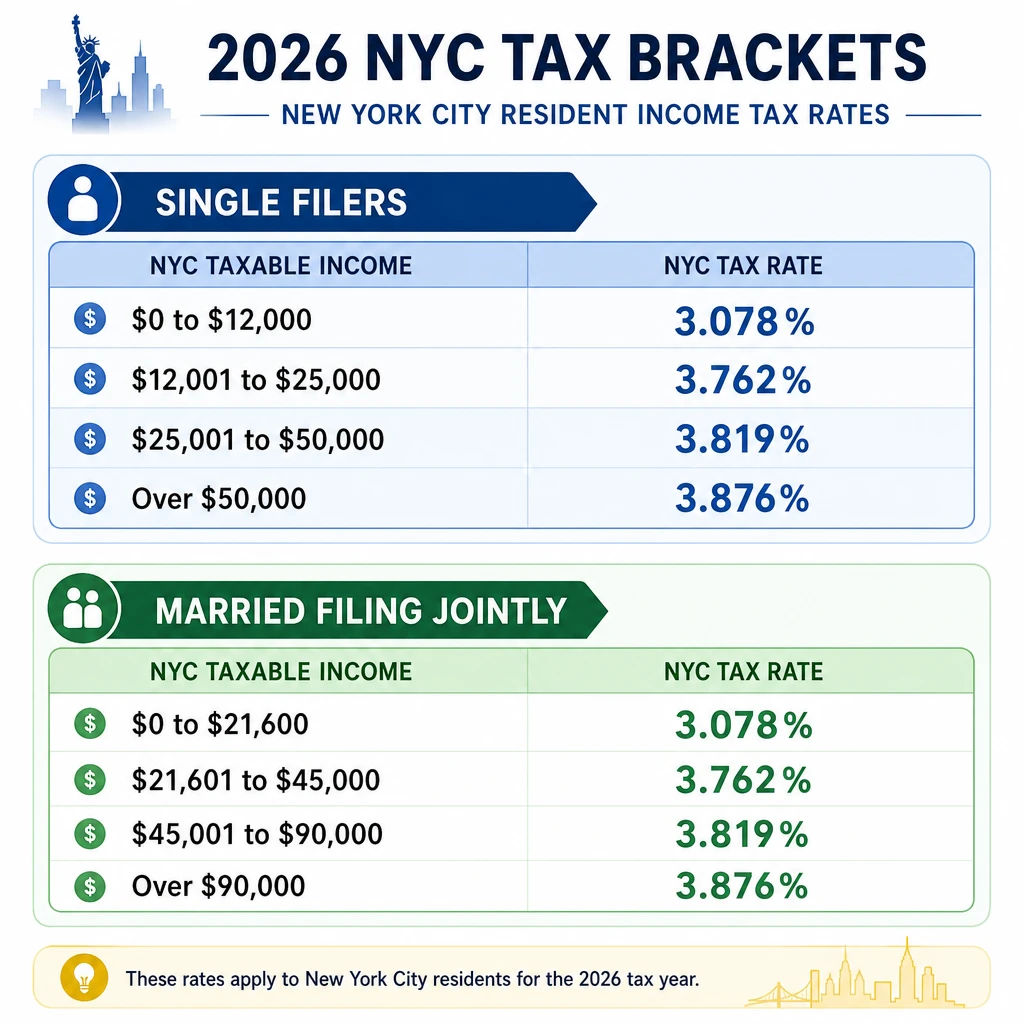

The 2026 NYC Income Tax Brackets

NYC uses four progressive brackets for city income tax. These rates apply to your NYC taxable income, meaning your income after deductions, not your gross salary.

The good news: these rates did not change from 2025. What you owe the city per dollar earned is the same as last year.

The married filing jointly brackets are wider, which means couples reach the top rate at a higher combined income than two single filers would. One more thing to know: if your NYC taxable income is under $65,000, you use the NYC tax table when you file. If it is $65,000 or more, you use the NYC tax rate schedule. Your tax software handles this automatically, but it is worth knowing.

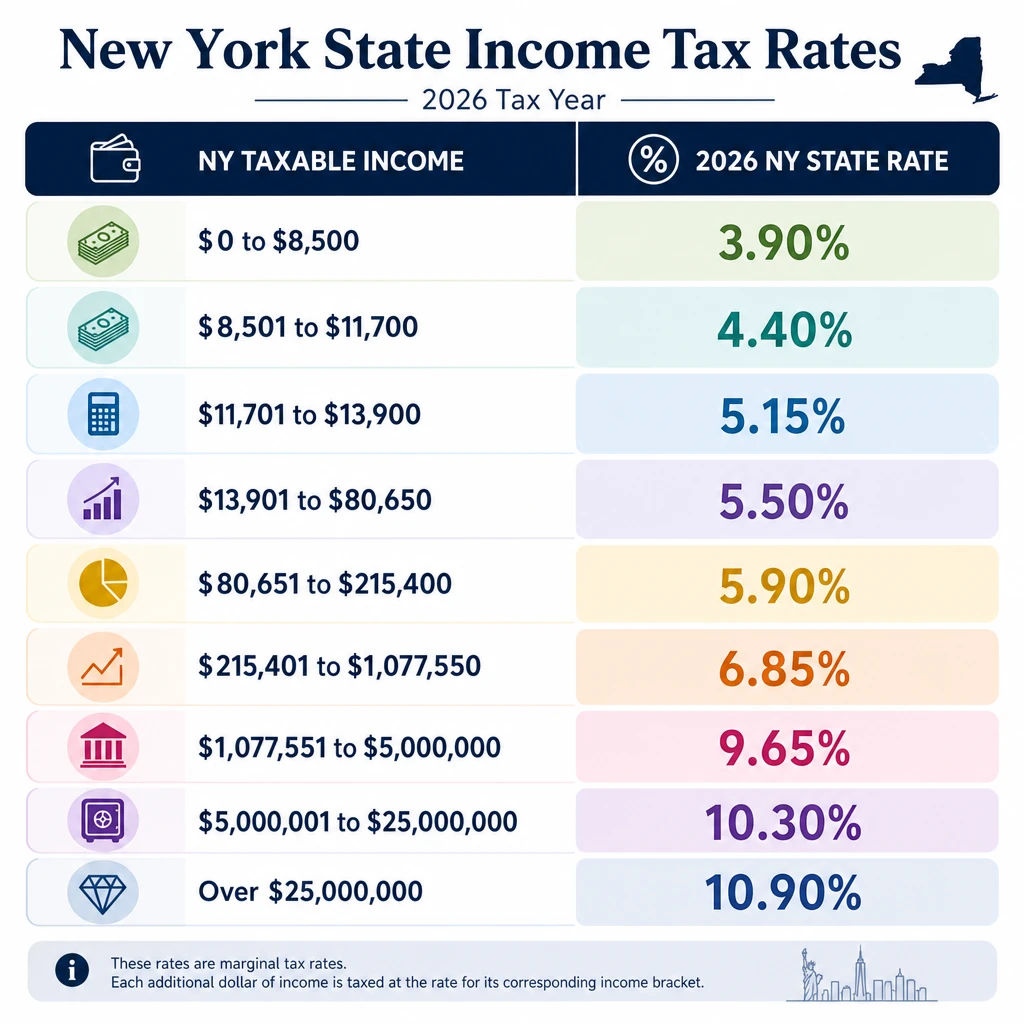

The 2026 New York State Tax Brackets

On top of the city tax, every NYC resident also pays New York State income tax. The state uses nine brackets ranging from 3.90% to 10.9% for 2026.

Governor Hochul's 2025-2026 budget reduced the bottom five brackets by 0.1% each, which delivered real savings to middle-class earners. If your income is under $215,400, you are paying slightly less in state tax than you did in 2025.

2026 NY State Tax Brackets for Single Filers:

One thing that catches people off guard: if your New York adjusted gross income exceeds $107,650, you also have to calculate a supplemental tax. This recapture provision phases out the benefit of the lower brackets as your income rises toward $265,400. It shows up as an extra line on your return and surprises a lot of filers who did not know it existed. Run your numbers before you file.

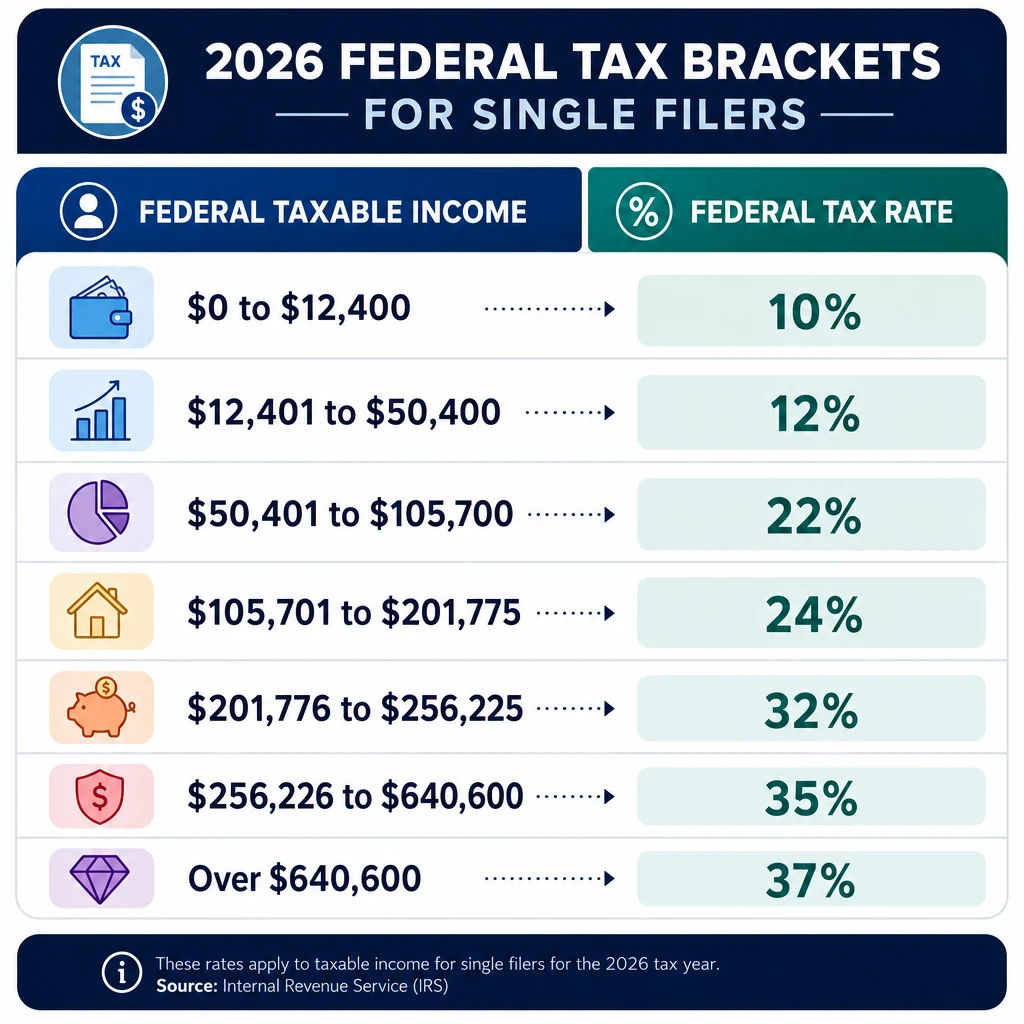

The 2026 Federal Tax Brackets

NYC residents pay all three layers: federal, state, and city. Federal brackets for 2026 were updated under the One Big Beautiful Bill Act, which adjusted the thresholds slightly upward compared to 2025.

2026 Federal Tax Brackets for Single Filers:

The federal standard deduction for single filers in 2026 is $15,000. That amount comes off your gross income before any of these rates apply, so your taxable income is already $15,000 lower than your total earnings before the calculation even starts.

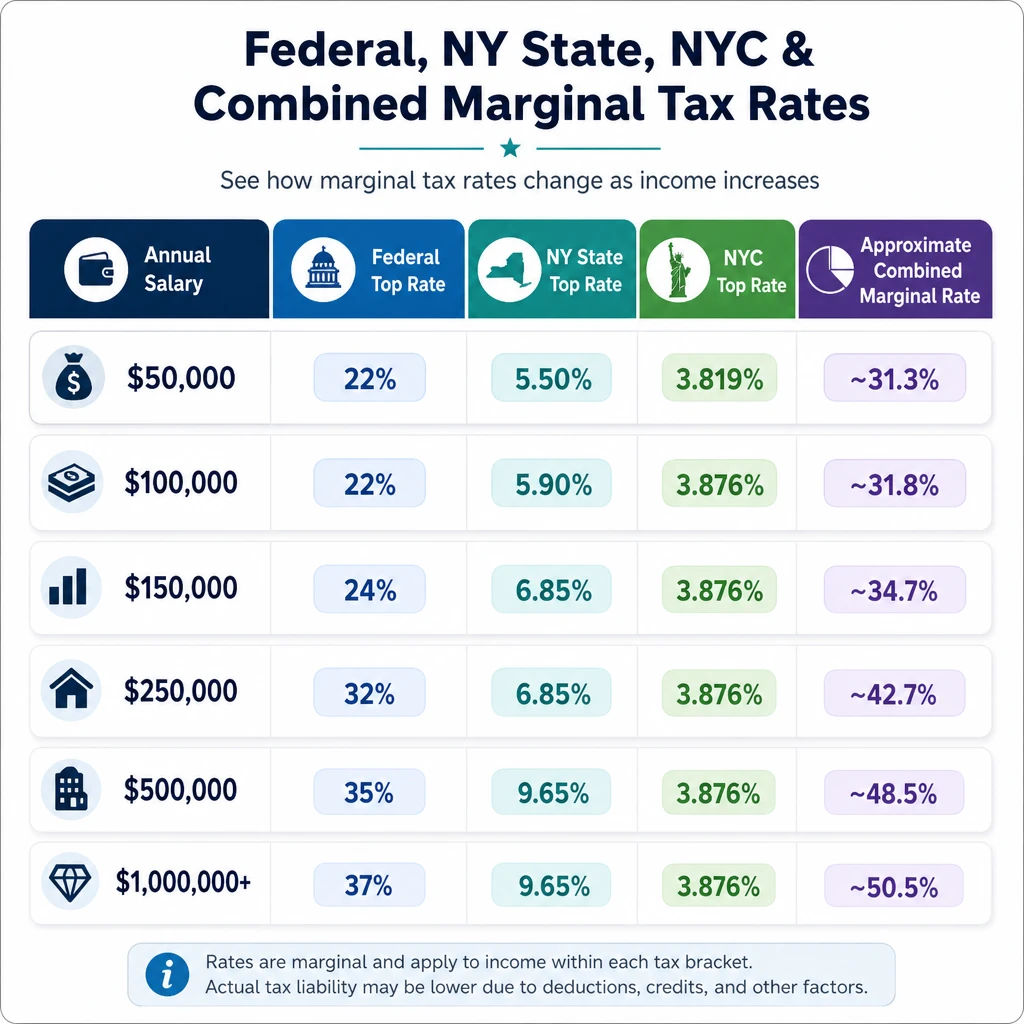

What Your Combined Tax Rate Looks Like in NYC

Here is where it gets real. NYC residents stack all three sets of brackets on top of each other. The table below shows the top marginal rate at different income levels when you add federal, state, and city together.

These are marginal rates on the top slice of income, not effective rates on everything you earned. Your actual bill will be lower than these percentages applied to your total salary. Get your exact combined effective rate at taxcalculatorny.com based on your real 2026 income and filing status.

Marginal Rate vs Effective Rate: Why It Matters

Your marginal tax rate is the rate on the last dollar you earned. Your effective tax rate is your total tax bill divided by your total income.

These two numbers are always different, and the effective rate is always lower.

A single NYC filer earning $100,000 is technically in the 22% federal bracket. But most of their income was taxed at 10% and 12% before reaching that level. Their actual effective federal rate ends up closer to 15% to 16%. The same logic applies to state and city brackets.

This is why the phrase "I got bumped into a higher bracket" almost never means what people think it means. Taking a raise, picking up freelance work, or selling an investment might push some of your income into a higher bracket. But the dollars already earned stay at their original rates. You always take home more money when you earn more.

What Changed in the 2026 NYC Tax Brackets vs 2025?

NYC city brackets stayed exactly the same. No rate changes, no threshold changes. The four tiers are identical to 2025.

At the state level, the bottom five New York State brackets each dropped by 0.1% as part of Governor Hochul's middle-class tax relief. An additional 0.2 percentage point reduction is being phased in over 2026 and 2027, so earners will see another small cut when they file taxes for the 2027 tax year.

Federal brackets shifted slightly upward for inflation under the One Big Beautiful Bill Act, which means more of your income falls into lower brackets compared to 2025.

One other update worth knowing: the Empire State Child Tax Credit increased from $330 to $500 per child for children ages 4 to 16 in 2026. If you have kids in that age range, that credit reduces your state tax bill directly when you file in 2027.

How to Figure Out Which Bracket You Are In

Working out your bracket takes five steps:

Start with your total gross income from all sources in 2026. Then subtract any pre-tax contributions you made, things like 401(k) deferrals, HSA contributions, and employer health insurance premiums. Subtract your standard deduction or total itemized deductions if you plan to itemize. What remains is your federal taxable income. Find that number in the federal bracket table above and you have your top federal bracket. Repeat the same process using New York's deductions for the state and city brackets.

The faster option: enter your 2026 income into the free calculator at taxcalculatorny.com and it applies all three sets of brackets automatically. You will have your federal, state, and city breakdown in under a minute.

5 Ways to Drop Into a Lower Bracket Before You File

Max out your 401(k). The 2026 contribution limit is $23,500 for workers under 50. Every dollar you contribute comes off your taxable income before any bracket calculation happens.

Make an IRA contribution before April 15, 2027. You can still contribute up to $7,000 for the 2026 tax year after December 31 has passed. If you are eligible for a deductible IRA, this reduces your taxable income directly.

Contribute to an HSA. If you had a qualifying high-deductible health plan in 2026, you can contribute up to $4,300 for self-only coverage or $8,550 for a family plan. HSA contributions reduce your federal adjusted gross income.

Deduct business expenses if you have self-employment income. Freelancers and side-hustle earners can deduct legitimate business costs before their net income hits the bracket calculation. Software, equipment, home office, and professional services all count if they are genuinely work-related.

Claim every credit you qualify for. The NYC school tax credit, the New York State Earned Income Tax Credit, and the Empire State Child Tax Credit all reduce your final tax bill. Credits are more valuable than deductions because they come off your actual tax owed, not just your taxable income.

Frequently Asked Questions

Does getting a raise push all my income into a higher bracket? No. Only the income above the bracket threshold gets taxed at the higher rate. Everything below that line stays taxed at the same rates as before. A raise always increases your take-home pay, even when it crosses a bracket line.

What is the highest NYC tax rate in 2026? The top NYC city rate is 3.876%, which applies to taxable income over $50,000 for single filers and over $90,000 for married filing jointly. This is on top of your New York State and federal taxes.

How does the NY State supplemental tax work for incomes over $107,650? If your New York adjusted gross income exceeds $107,650, you calculate an extra tax that phases out the benefit of the lower brackets you used on the income below that threshold. This recapture continues until around $265,400 for single filers. It shows up as a separate line on Form IT-201.

What is the standard deduction for NYC taxes in 2026? The federal standard deduction is $15,000 for single filers in 2026. New York State uses $8,000 for single filers and $16,050 for married filing jointly. NYC city tax generally follows the same deduction amount as the state return.

I am married filing jointly. How do my NYC brackets work differently? The income thresholds are wider for married filers. You pay the lowest NYC rate on the first $21,600 of combined income instead of $12,000, and you do not hit the top 3.876% rate until your combined taxable income exceeds $90,000. This generally reduces the overall city tax burden compared to two single filers with the same combined income.

Tax rates in this article reflect the official 2026 tax year rates from the New York City Department of Finance, the New York State Department of Taxation and Finance, and the IRS. All figures are estimates for informational purposes. Speak with a licensed tax professional for guidance on your specific situation.