New York State vs NYC Tax in 2026: What's the Difference?

Confused about NY State tax vs NYC tax in 2026? We break down exactly who pays what, the rates, and how much each one takes out of your paycheck. (150 chars)

A lot of people who move to New York City for work assume there is one "New York tax." There are actually two, and they work very differently. One applies to nearly everyone who earns money in the state. The other is a separate charge that only people who live inside the city limits pay.

The Short Answer

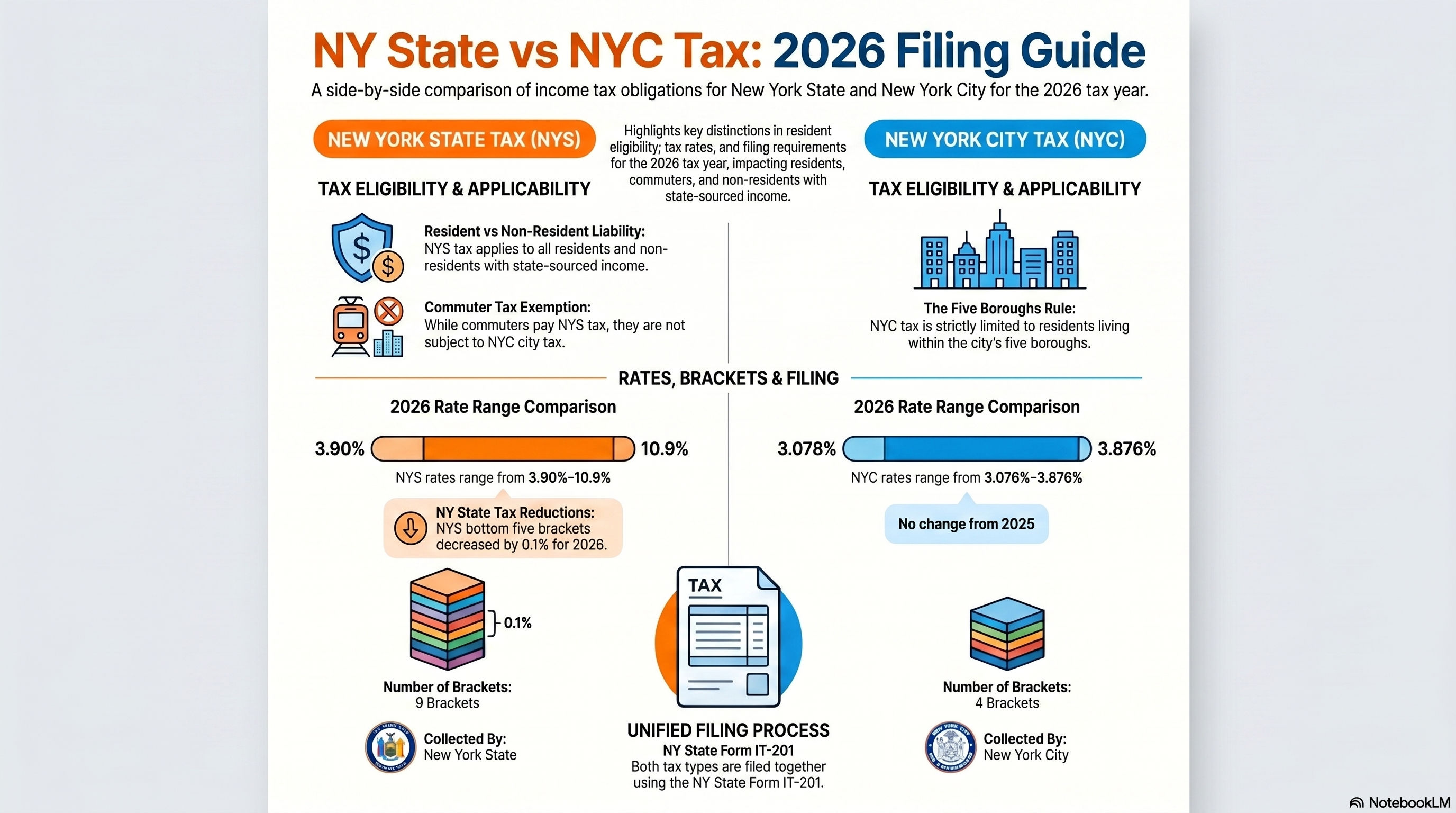

New York State income tax applies to everyone who earns income in New York State. That includes people living in Manhattan, people living upstate in Buffalo, and people who live in New Jersey but earn their paycheck from a New York employer.

NYC city income tax is an additional, separate tax that only applies to people who actually live inside the five boroughs: Manhattan, Brooklyn, Queens, The Bronx, and Staten Island.

If you live in Hoboken and commute to a Midtown office every day, you pay New York State tax on those wages. You do not pay NYC city tax. That one distinction saves some commuters thousands of dollars a year.

What Is New York State Income Tax?

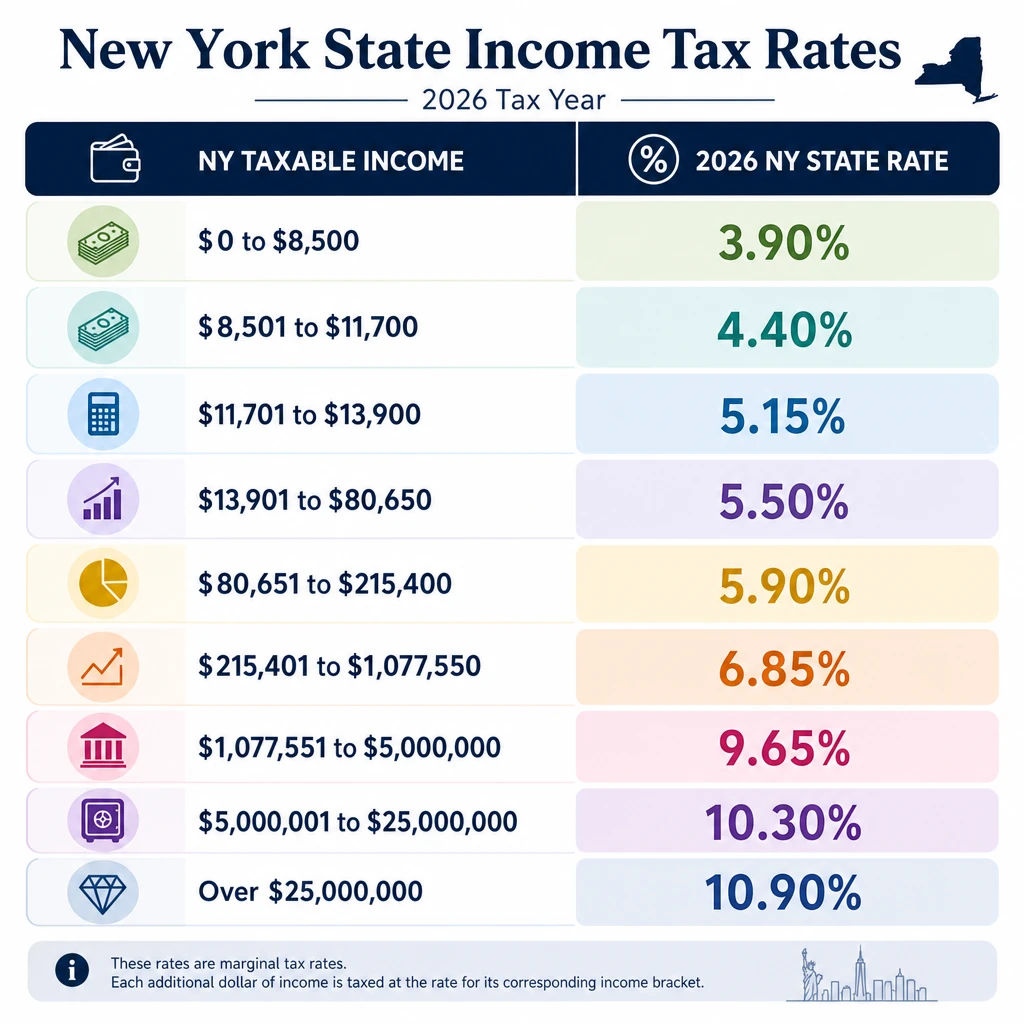

New York State income tax is a progressive tax with nine brackets. For 2026, rates range from 3.90% at the low end to 10.9% at the very top.

Governor Hochul's 2025-2026 state budget reduced the bottom five brackets by 0.1% each, delivering nearly $1 billion in relief to over 8.3 million filers. For most middle-class earners, this showed up as slightly larger paychecks starting in early 2026 when the updated withholding tables took effect.

Here are the 2026 New York State income tax brackets for single filers:

The standard deduction for New York State is $8,000 for single filers and $16,050 for married filing jointly. One thing to know: if you earn over $107,650 as a single filer, benefit recapture rules gradually phase out the advantages of the lower brackets as your income rises toward $265,400.

What Is NYC Income Tax?

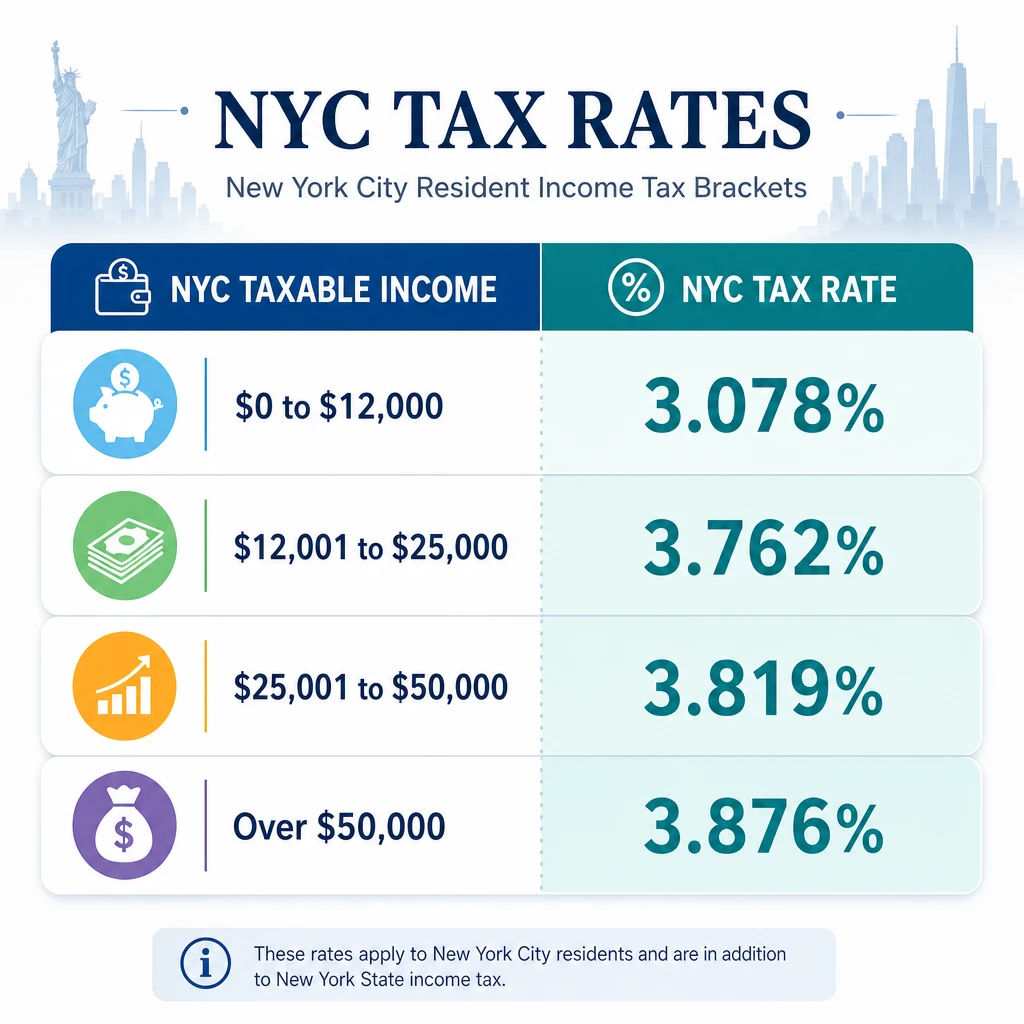

NYC city income tax is a local tax charged on top of your New York State tax. It is not a federal thing. It is not a state thing. It is a tax set by New York City and collected specifically from people who live within the five boroughs.

The 2026 city tax rates range from 3.078% to 3.876%. These rates did not change from 2025.

Here are the 2026 NYC income tax brackets for single filers:

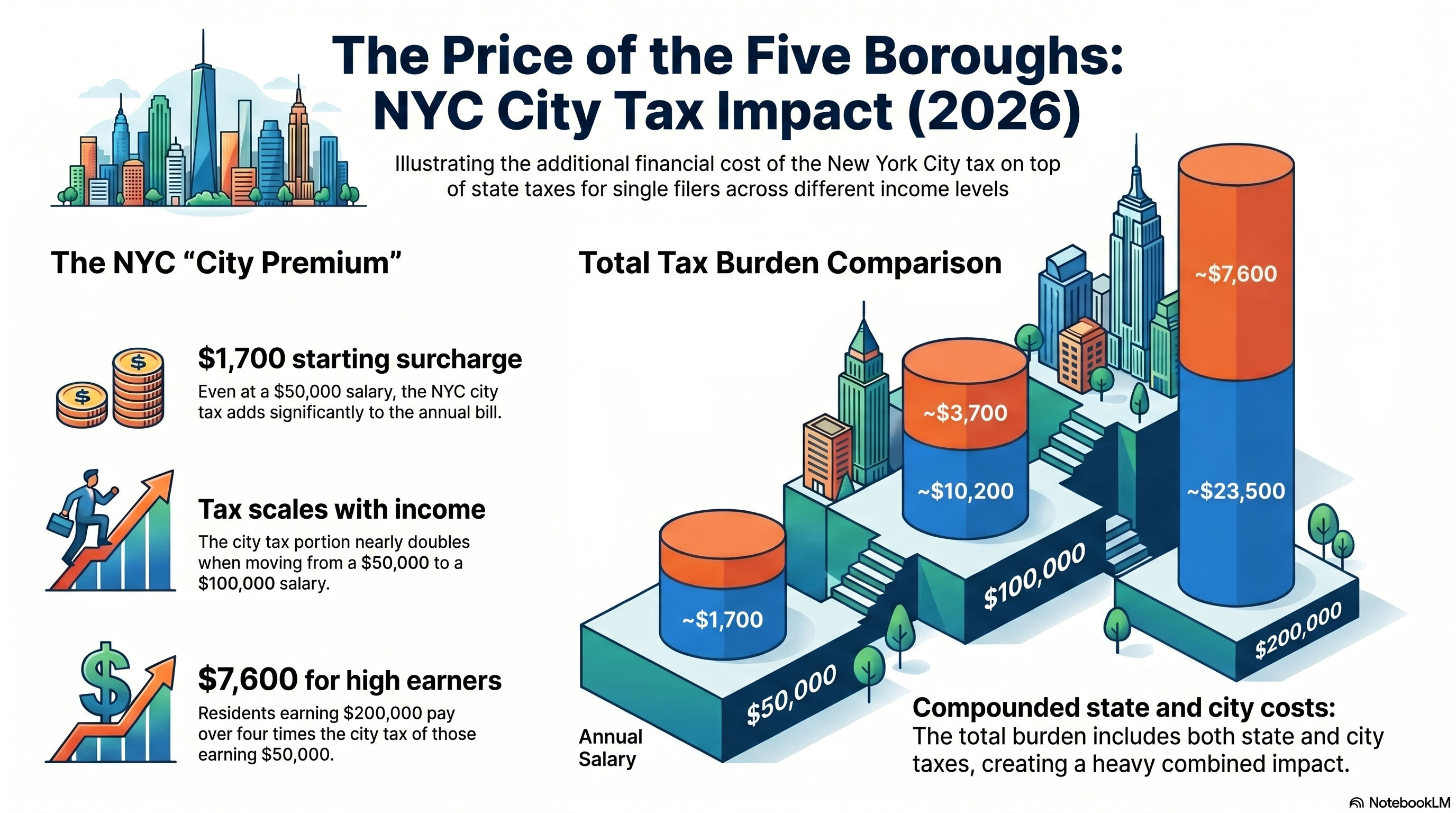

On a $100,000 salary, city tax adds roughly $3,700 to your annual bill. On $150,000, it adds around $5,600. That is money you keep entirely if you live outside the city limits.

NY State Tax vs NYC Tax: Side by Side

The last row surprises a lot of people. You do not file a separate return for NYC city tax. Both taxes get reported on the same New York State Form IT-201. The city tax section is just a separate calculation within the same document.

How Much Does NYC Tax Actually Add to Your Bill?

Here are estimates for single filers in 2026 claiming the standard deduction. These numbers show what living in NYC costs you specifically in city tax compared to living just outside the five boroughs.

The city tax column is what someone living in Nassau County, Westchester, or New Jersey does not pay. At $100,000, that is $3,700 a year in extra taxes just for living in the city. Get your exact number for your 2026 income at taxcalculatorny.com.

Who Pays NYC Tax and Who Does Not?

You pay NYC tax if you lived in Manhattan, Brooklyn, Queens, The Bronx, or Staten Island for any part of 2026. Even one day of residency can create a city tax obligation for that period.

You do not pay NYC tax if your home is in New Jersey, Connecticut, Long Island, Westchester, or anywhere outside the five boroughs, even if you work in the city every day.

Partial-year residents only owe city tax for the months they actually lived in NYC. If you moved from Brooklyn to Hoboken in July 2026, you owe city tax on your income from January through July and nothing for August through December.

Remote workers are a more complicated case. If you live outside NYC and work remotely for an NYC-based company, you generally do not owe the city tax. But New York State's "convenience of employer" rule may still require you to pay state income tax on that income, even if you never set foot in a New York office. That rule catches a lot of people off guard.

Does Living Outside NYC Actually Save You Money?

Yes, and the savings are more significant than most people realize.

Someone earning $100,000 who lives in New Jersey instead of Manhattan saves roughly $3,700 per year in city tax alone. Over 10 years, that is $37,000 in additional take-home pay before accounting for any salary growth.

The practical comparison is more complicated. New Jersey has its own state income tax. Commuting from Hoboken or Jersey City costs money. Some people pay more in monthly transit costs than they save in city tax. And rent in certain NJ neighborhoods has risen significantly as people chase exactly this savings.

The point is not that living outside the city is always the better financial move. It is that the city tax gap is real and worth factoring into the decision.

What Changed for 2026 That Affects Both Taxes?

Three updates are relevant when you file your 2026 return in 2027.

NY State bracket reductions. The bottom five state brackets each dropped by 0.1% under the 2025-2026 state budget. This is a genuine reduction, not just an inflation adjustment. If you earn under $215,000, your effective state rate is slightly lower than it was for the 2025 tax year.

Updated withholding tables. New York State updated its payroll withholding tables on January 1, 2026. Many employers adjusted paychecks at the start of the year to reflect the new rates, which is why some workers noticed a small increase in their take-home even without a raise.

NYC city tax rates stayed flat. The four NYC brackets are unchanged from 2025. No new rates, no new thresholds. The city tax is the same as it was last year.

Federal changes under the One Big Beautiful Bill Act also updated federal brackets and standard deductions for 2026. These federal changes ripple through to your state calculation, since New York State starts its math from your federal adjusted gross income.

What Is Your Combined Tax Rate as an NYC Resident?

Most people want to know their total effective rate across all three layers, not just one piece at a time.

For a single filer earning $100,000 in NYC, the combined effective rate across federal, state, and city taxes typically lands between 30% and 34%. At $200,000, that climbs to roughly 38% to 42%. For earners above $1 million, the stacked marginal rate can exceed 52% when you add the 37% federal top rate, 9.65% state rate, and 3.876% NYC city rate together. That puts New York City among the highest combined tax jurisdictions in the country.

The gap between being an NYC resident and a non-city New York State resident is primarily that 3.078% to 3.876% city layer. At high incomes, removing that layer makes a meaningful difference.

Ready to see your exact combined rate for 2026? The free calculator at taxcalculatorny.com breaks down your federal, state, and city taxes side by side before you file in 2027.

Frequently Asked Questions

Do I pay NYC tax if I live in New Jersey but work in Manhattan? No. NYC city income tax is based on where you live, not where you work. If your home is in New Jersey, you skip the city tax. You will still owe New York State income tax on the wages you earn there, and New Jersey will tax your income too. Most states give you a credit to prevent being taxed twice on the same money.

What form do I use for both NY State and NYC taxes? Both go on the same form: New York State Form IT-201. You do not file a separate return just for city tax. The IT-201 has a section where NYC residents calculate their city tax as part of the same filing.

If I moved out of NYC in 2026, do I owe city tax for the whole year? No. You owe NYC city tax only for the months you actually lived in the five boroughs. File as a part-year NYC resident on your 2026 return and calculate tax only on the income earned during your time in the city.

Can I avoid NYC tax by having my employer use a different address? No. New York City and State conduct residency audits and look well beyond what address your employer has on file. If you actually lived in the city, you owe the tax. Listing a different address can lead to back taxes, penalties, and interest on top of what you originally owed.

Does NYC tax apply to retirement income? New York State exempts Social Security and most pension income from state tax. NYC follows the same general rules for city tax. Distributions from 401(k) accounts and traditional IRAs may still be subject to both state and city tax depending on your situation.

Tax rates in this article reflect the official 2026 tax year rates from the New York State Department of Taxation and Finance and the New York City Department of Finance. Figures are estimates for informational purposes only. For guidance specific to your situation, speak with a licensed tax professional.